- Home

- Bad Credit Car Finance

Bad credit car finance with Luv

- Vehicles from trusted UK dealers

- Free quote - no impact to your credit score

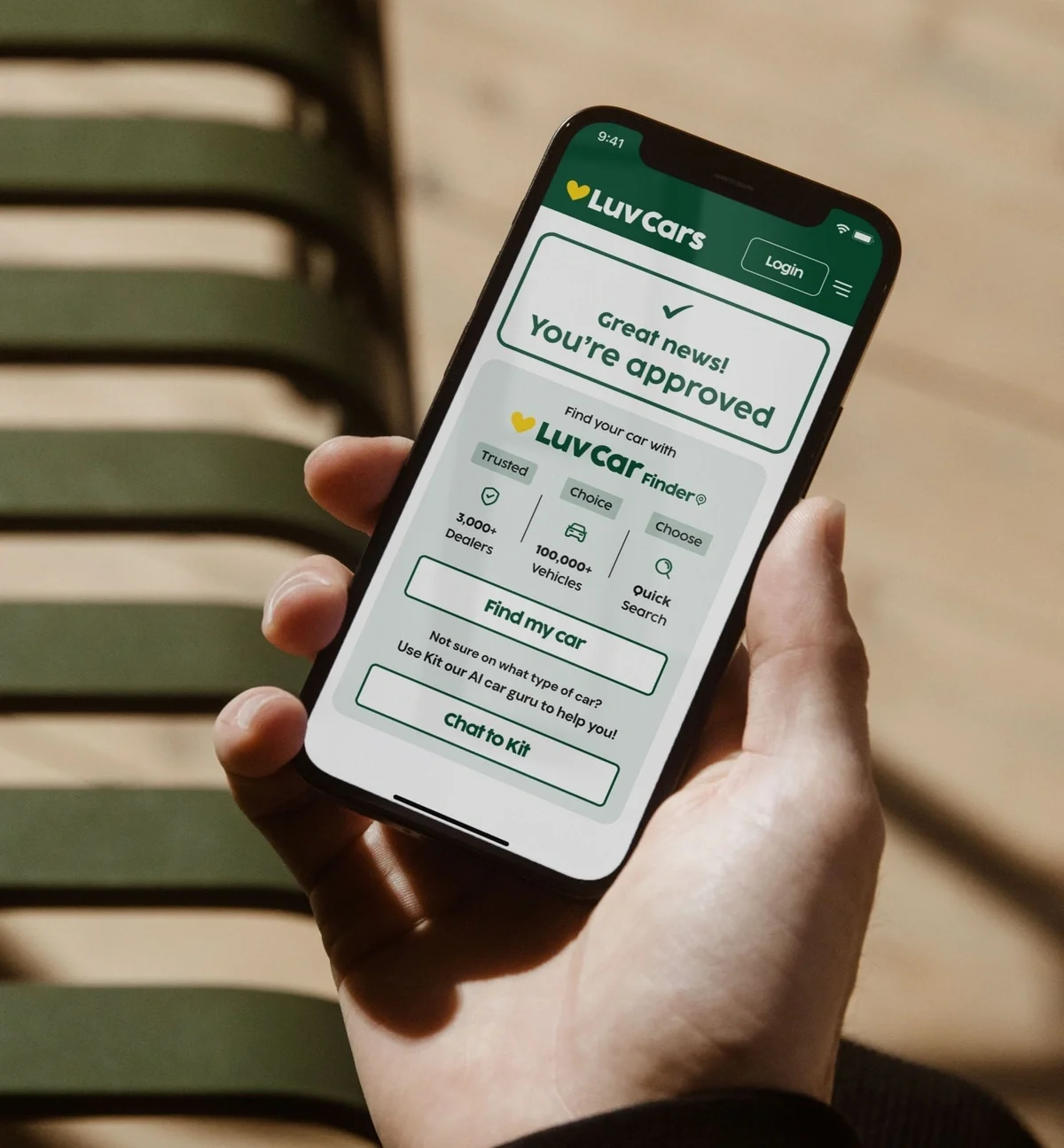

- Get approved in minutes

Can I get car finance with bad credit?

Getting car finance with bad credit is possible, even if you've missed payments, had a CCJ, or defaults on your account in the past. However, you might find yourself with fewer options and at higher interest rates – but there are specialist lenders who help people with poor credit get approved for car finance.

If you have bad credit, it’s important to understand your credit file, and to take the right steps in getting the best car finance for your own personal situation. Check your credit report and make sure the information is correct – if you spot a mistake, raise a dispute.

You should also shop around for your best options, and use an eligibility checker to see your chances of being accepted before applying – that way you can avoid rejection which can leave a mark on your credit file.

Apply in just 60 seconds

Comparing finance with Luv Cars is quick and easy.

1. Get approved

Get your personalised car finance quote and approval in principle in minutes using our smart search tool.

2. Choose your car

Once approved, find your car by using LuvCar finder. Showing you 1000’s of options from our approved dealers.

3. Drive away... and Luv it!

We’ll sort everything out. You just turn up and drive away.

Frequently Asked Questions

Bad credit can mean a few things, and can include missed or late payments, County Court Judgements (CCJs), defaults on loans and credit cards, bankruptcy, or Individual Voluntary Arrangements (IVAs). You can even mean having little or no credit history, as banks and lenders don’t have enough information to base their decision on.

It’s also important to remember that there isn’t just one credit score – instead, there are three main Credit Reference Agencies or CRAs (TransUnion, Equifax, and Experian), with each one having a different score and a different way of calculating it.

You can check your credit report for free through apps like TotallyMoney for your TransUnion score, or CredAbility for your Equifax one – or directly with Experian.

Before you apply for any loan or credit, it's always worth checking your report. That way you can check that the information is correct and up to date, and see what might be holding you back. If you find an error, you can raise a dispute with the relevant agency.

When shopping around for car finance, it’s important to use tools like eligibility checkers which use a 'soft search', as they won't impact your credit score at all.

However, making a full application can, as lenders will use a 'hard search'. This can show on your credit file, and making multiple applications in a short space of time could affect your chances of borrowing in future.

If you have bad credit, it’s likely that you’ll have fewer options, and with higher Interest rates. That’s because lenders will see you as more of a risk. However, rates can vary depending on your circumstances, such as how much you want to pay, and over how long.

Shop around and compare your options, as you might find that using a specialist lenders and putting down a bigger deposit can help you get a better deal.

This will usually depend on your credit history, how much you would like to borrow, and the type of car finance you’re taking out. Some car finance lenders offer no-deposit deals, but it’s worth remembering that a deposit can often improve your chances of getting approved, and might help you get a lower interest rate.

There are three main types of car finance available:

- Hire Purchase (HP)

- Personal Contract Purchase (PCP)

- Personal car loans

Each type of finance works in a different way.

With HP, you make fixed monthly payments over a set amount of time, and own the car when you've paid everything off.

With PCP, your monthly payments are often lower, but if you want to own the car at the end of the agreement, you'll need to make a final ‘balloon payment’.

With a personal loan, you borrow the money to buy a car, which you then own, and you make fixed monthly payments over the duration of the agreement.

It is still possible to get car finance after bankruptcy, but you’re likely to have fewer options, and you will probably pay a higher interest rate.

Having a County Court Judgement (CCJ) won't automatically stop you from getting car finance, but it can make it harder. When applying for car finance, lenders will look at how recent the CCJ is, how much it was for, and whether you’ve satisfied it (paid off).

If the CCJ is older, or you’ve settled it, you might have more options. There are some specialist lenders who will offer finance to people with CCJs, so make sure you compare all your options.

There are a few things that can help your application, such as getting on the electoral roll at your current address, checking your credit report for incorrect information, and reducing how any existing debts where you can.

It's also worth thinking about the car you need, and can afford, and not the one you dream of. That's because being realistic and staying within your budget can mean you’re more likely to get accepted. If you can, save up for a deposit as this can show lenders that you're able to manage your money, and will reduce the total amount you need to borrow.

Having someone who can make your payments if you can't can help you to get approved, or get better rates. However, it’s important that they know what they’re getting themselves in for because it can be a big responsibility, making them legally liable if you miss payments.

If you're struggling to keep up with repayments, then contact your lender right away. They might be able to offer support by adjusting your payment plan, which can give you some extra breathing space.

Remember that missed payments can damage your credit score, and might lead to your car being repossessed.

If you make all your payments on time, car finance can help you to build your credit score. That’s because it shows lenders you’re able to manage credit responsibly, even if you've had problems in the past.

Just make sure you can afford the payments before you commit, as missing them can damage your credit file.

Your credit file shows six years of borrowing history, meaning it’s important to start taking the right steps to improve it sooner rather than later.

Your more recent history will usually have more of an impact, so your situation can improve even before the six years are up.

When applying for car finance you’ll need proof of identity, proof of where you live, and proof of how much you earn. If you're self-employed, you'll usually need to share tax returns or accounts for the past few years.

If you have bad credit, then it’s worth trying to stay within your budget, as the higher the loan amount, the harder it can be to get approved, and the more money it could cost you in the long term.

It’s also worth remembering that older cars with high mileage might also be harder to finance and insure, as they're seen as less reliable.